Custodial Roth IRA’s: A Smart Start for Kids & Grandkids?

A Custodial Roth IRA is a retirement account created for a minor with the help of a parent, grandparent, or guardian. The adult oversees the account until the child reaches adulthood, at which point the young person takes full ownership. It's one of the most powerful tools to grow wealth early using compound interest and tax-free growth.

💼 Eligibility & Contributions

🛠️ Earned Income Required

To contribute, the child must have reportable earned income: wages, tips, self-employment income (like babysitting, yard work, acting gigs, or small business revenue). Gifts or allowance do not count.

📊 Annual Contribution Limits (2024–2025)

- Maximum: $7,000, or

- The total earned income for the year, whichever is less

Example: If your child earns $2,500 mowing lawns, you can contribute up to $2,500 for that year.

👨👩👧 Who Can Fund It?

Anyone (usually parent, grandparent, relative) can fund the account. But the contribution cannot exceed what the child actually earned.

🛡️ Custodian Responsibilities

The adult custodian is in charge of:

- Opening the account

- Choosing and managing investments

- Making contributions (based on the child’s income)

- Ensuring IRS rules are followed

Control of the account shifts to the child when they reach the age of majority—usually 18 or 21, depending on your state.

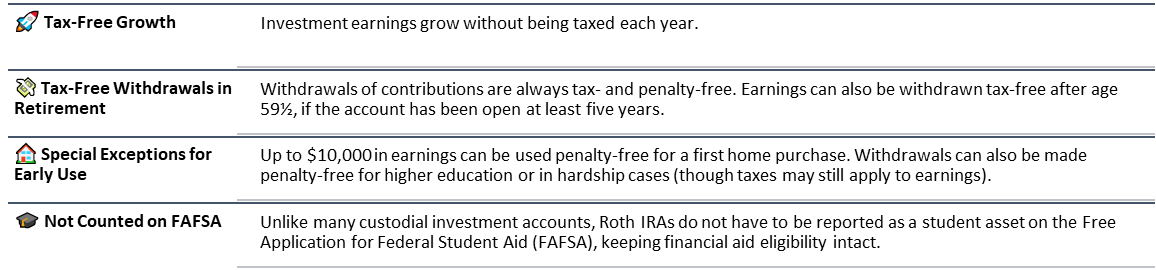

📈 Benefits of a Custodial Roth IRA

🧠 Key Considerations

Topic | Notes |

Ownership Transfer | Full control is passed to the child at the legal age of majority. |

Contribution Limits | Limits apply per child and do not reduce a parent’s own Roth IRA limit. |

Withdrawal Flexibility | Contributions can be withdrawn at any time without tax or penalty. |

Recordkeeping | Maintain documentation of the child’s earned income (paystubs, invoices, etc.). |

🏁 How to Get Started

1. Choose a provider:

Select a brokerage or financial institution that offers custodial Roth IRAs (we can help with this and administer many types of institutions)

2. Gather details:

You’ll need Social Security numbers and other information for both the minor and the custodian.

3. Open the account:

The custodian will complete paperwork, link a funding source, and choose investment options.

💬 Example Scenario

Ella, age 16, earns $3,500 from a part-time summer job. Her parents open a Custodial Roth IRA and contribute the full $3,500 on her behalf. If invested wisely, this early start could grow to six figures by the time Ella reaches retirement, even without another dollar added.

🧭 Why This Matters

Starting young gives investments time to grow. Even modest early contributions can become life-changing thanks to compound growth and the Roth IRA’s tax advantages.

Let McFee Financial Group help you build a legacy of financial wisdom and opportunity.

This information is for educational purposes only and is not tax or investment advice. Consult a tax advisor before making decisions.

To qualify for the tax-free and penalty-free withdrawal or earnings, a Roth IRA must be in place for at least five tax years, and the distribution must take place after age 59 ½ or due to death, disability, or a first-time home purchase (up to a $10,000 lifetime maximum). Depending on state law, Roth IRA distributions may be subject to state taxes.

Cetera Advisor Networks LLC exclusively provides investment products and services through its representatives. Although Cetera does not provide tax or legal advice, or supervise tax, accounting or legal services, Cetera representatives may offer these services through their independent outside business. This information is not intended as tax or legal advice.