Investment Tax Series: Part I The Governmental Taxes on Investing How They Can Eat Away Your Wealth

When most people think of the taxes associated with investing, their mind immediately jumps to April 15th and capital gains taxes. While government taxes are certainly a real cost, they’re just the beginning. In reality, investing comes with a variety of "hidden taxes". For example: mental, emotional, social … And these can have just as much impact on your wealth and your experience.

At McFee Financial Group, we believe understanding these unseen costs is key to long-term success. In this series, we’ll break down each type of investment tax, how they affect you, and how we work to minimize their burden.

First up: the government tax - the one you can actually measure.

“It’s not what you make, it’s what you keep.” — David Bach

When it comes to investing, many focus only on their returns. But the real game-changer?

It’s what you keep after taxes that defines your financial future.

Executives and business owners usually aim to be more intentional when it comes to government taxes; preserving more of the wealth you’ve worked so hard to build.

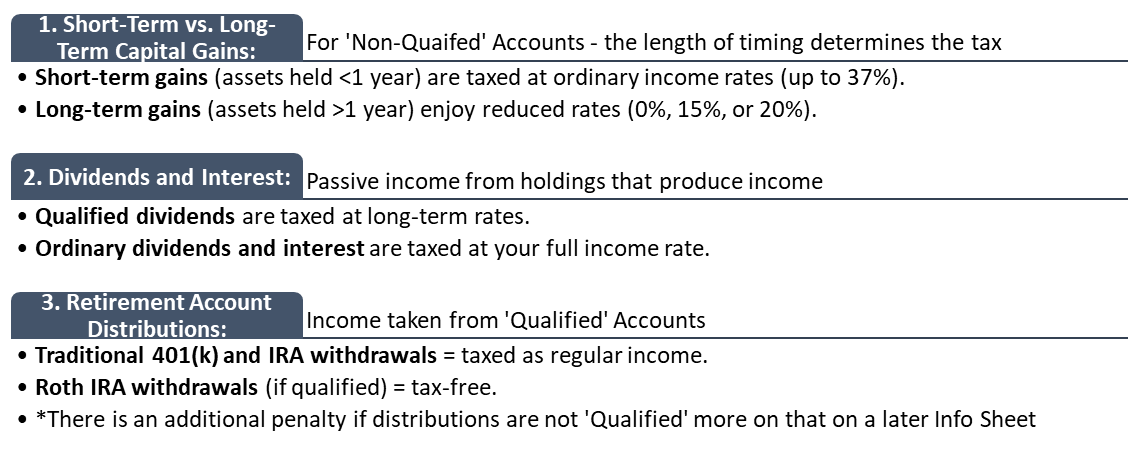

There are many other account types and nuances to consider, but we will stick with these three main ones for now. The main point is that without proper tax planning, government taxes could cost you thousands (or even millions) over your lifetime.

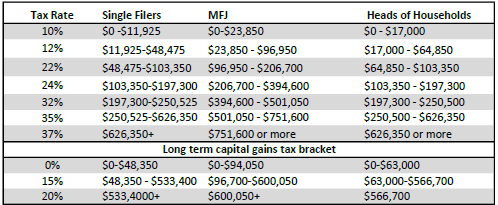

From the “McFee Financial Group 2025 Limits, Maximums, and Phaseout Reference Sheet"

Below is an excerpt from our Resource summarizing main tax brackets and categories for the year. This list was compiled by the McFee Financial Group Team, and holds a few examples of taxation of households in the US.

Top 3 Takeaways:

- Long-term investing can dramatically lower your tax bill.

- Choosing the right investment accounts shields more of your returns.

- Working with a tax-aware wealth advisor is critical for cohesive planning.

To qualify for the tax-free and penalty-free withdrawal or earnings, a Roth IRA must be in place for at least five tax years, and the distribution must take place after age 59 ½ or due to death, disability, or a first-time home purchase (up to a $10,000 lifetime maximum). Depending on state law, Roth IRA distributions may be subject to state taxes.

Distributions from traditional IRAs and employer sponsored retirement plans are taxed as ordinary income and, if taken prior to reaching age 59 ½, may be subject to an additional 10% IRS tax penalty.

Cetera Advisor Networks LLC exclusively provides investment products and services through its representatives. Although Cetera does not provide tax or legal advice, or supervise tax, accounting or legal services, Cetera representatives may offer these services through their independent outside business. This information is not intended as tax or legal advice.