Should I Fill My Tax Bracket with Roth Conversions?

What Does “Filling a Tax Bracket” Mean?

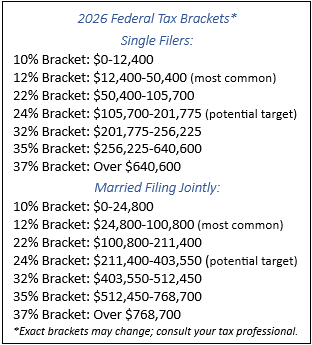

Filling a tax bracket refers to strategically converting Traditional IRA (Pre-Tax) funds to a Roth IRA; up to the top of your current tax bracket without spilling into the next one. This approach may help maximize your tax efficiency in certain situations. For example, if the top of your tax bracket is $95,000, and your current taxable income is $75,000, you could convert ~$20,000 of traditional IRA funds to a Roth IRA this year while remaining within the same tax bracket.

Who Should Consider This Strategy?

Filling your tax bracket with Roth conversions works well for people who:

- Anticipate a Higher Bracket Later: If your taxable income is likely to increase in retirement due to pensions, Social Security, or Required Minimum Distributions (RMDs), converting now allows you to lock in today’s lower tax rates.

- Anticipate the Same Bracket Later: Even if you expect to remain in the same bracket, converting now avoids the risk of future tax rate increases.

- Reducing RMD’s: This strategy helps you achieve tax-free growth in a Roth IRA and reduce future taxable RMDs from traditional accounts.

- Taxable Estate Planning: If you have no use for the funds, an you have working heirs, it may be a more tax-efficient way to pass assets to the next generation.

How to Convert to a Roth IRA

- Partial/Whole Traditional IRA Conversion: Convert a portion or all of your existing Traditional IRA to a Roth IRA, staying within your desired tax bracket.

- 401(k) Roth Conversion (aka Mega-Back-Door Roth): Use your employer’s 401(k) plan to move funds into a Roth option, provided you’re eligible for in-service rollovers, and you are over age 59.5 to potentially avoid penalty.

Why Roth Conversions Aren’t for Everyone

While a Roth IRA Conversion is a popular strategy, it’s not ideal for everyone if your:

- Already in a high tax bracket

- RMD’s fit in your income plan for a long period of time, or you plan to utilize QCD’s

- All income planning is needed for lifestyle up to a certain tax bracket

- Medicare IRMAA Limits are exposed

- Consulting/Part-time work adds too much or unpredictable income to target a tax bracket

- Yours heirs are in a very low tax bracket, and will pay less income taxes on the RMD/10-year Inherited IRA Account Liquidation Rule.

- You are under age 59.5, and don’t want to pay tax out-of-pocket to cover the tax difference (Then 10% penalty is owed)

Other ways to Use Roth IRA’s

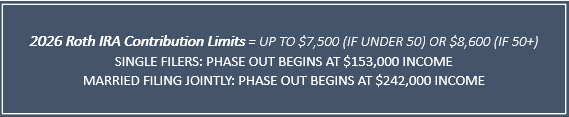

- Contribute to your own Roth IRA if you qualify

- If for Estate Purposes, Contribute directly to a family member’s Roth IRA

Convert unused 529 Funds to Roth IRA’s for the beneficiaries (if qualified and under the limit)

Ready to Optimize Your Roth Conversion Strategy?

At McFee Financial Group, we help clients navigate Roth IRA conversions and other wealth-building strategies. Reach out if you’d like us to help guide the best path forward for your unique financial goals.

📞 Call: (763) 425-5777 +1 (763) 363-2332 🌍 Visit: www.mcfeefinancial.com